Economics 101: Understanding the Term Structure of Interest Rates and the Yield Curve

Written by MasterClass

Last updated: Oct 12, 2022 • 6 min read

When you invest your money into interest-bearing security, the amount of interest paid will vary depending on the length of the investment term. In other words, a savings bond with a one year term may pay a fairly low interest rate, but if you invest your money in a bond with a ten-year term, you may receive a higher rate of interest. When we discuss how the length of investment affects a security’s interest rate, we are talking about the security’s term structure.

Learn From the Best

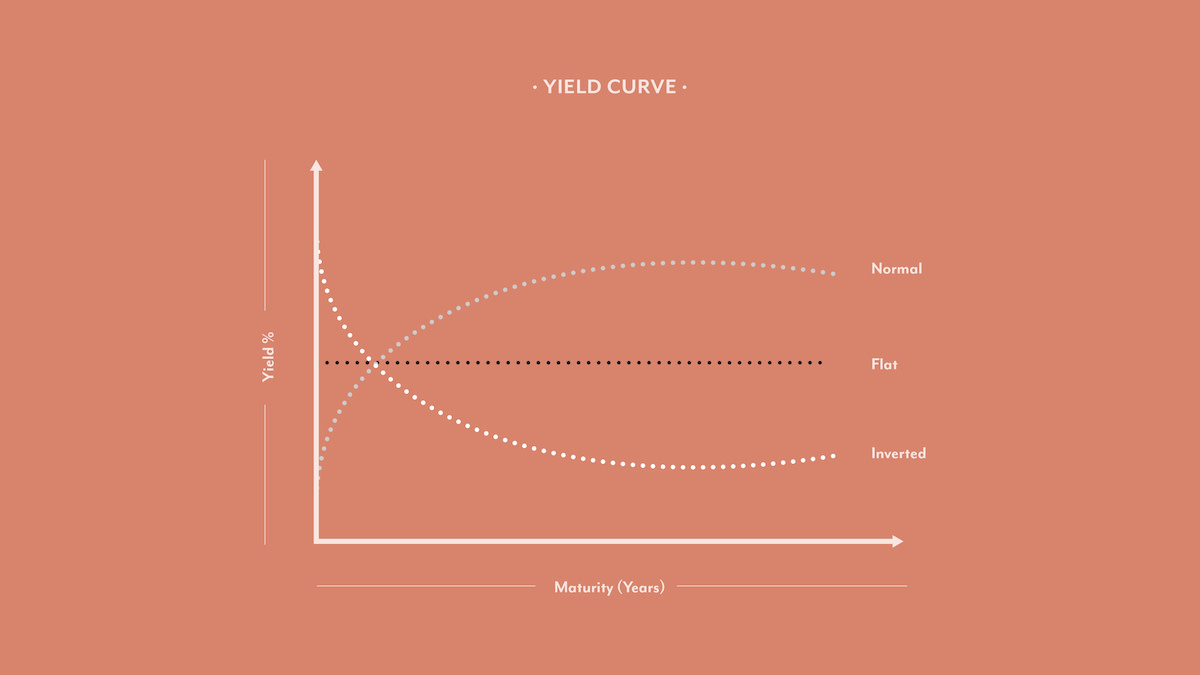

What Is the Yield Curve?

The yield curve is a line that represents the yield (or amount of interest paid) by various bonds and investment notes that achieve maturity at varying dates.

The yield curve can be graphed on a standard XY axis.

- The X-axis represents the borrowing period (sometimes known as the maturity) of a particular loan, bond, or treasury note (all of which are known as debt securities). There is a wide range of such debt securities available on the market, whether that’s a 10-year treasury note, a five-year note, a two-year note, a one-year note, or even something much shorter, like a three-month note that reaches maturity in just over 90 days.

- The Y-axis represents the yield of the security. The yield is the percent interest that is paid when the bond, loan, or note reaches maturity. This is based on the principle that if you purchase a 10-year note from the U.S. Treasury that promises 5% interest, you will only receive that 5% interest if you wait the full 10 years to collect your money.

U.S. Treasury bonds do not promise high-interest rates, but they are considered very reliable. If you purchase a treasury note that promises a 5% interest rate upon maturity, you can confidently expect to receive your 5% payment at the prescribed time.

How Does the Yield Curve Behave?

The yield curve most commonly analyzed by market analysts compares the interest rates paid by five types of U.S. Treasury debt: the three-month, two-year, five-year, 10-year and 30-year notes.

- In a normal yield curve, the yield paid by bonds increases with length. Therefore, a 30-year bond pays more than a 10-year bond, which pays more than a five-year bond, which pays more than a two-year bond, which pays more than a three-month bond. Typically the yield rapidly leaps from a three-month bond to a five-year bond. The curve flattens out a bit from there, but in normal conditions, long-term yields will still be higher than short-term yields.

- In an inverted yield curve, the bond market’s short-term rates are higher than its long-term rates. That means, for instance, that a two-year treasury note will offer a higher yield than a five-year note. Under normal conditions, however, the longer-term bond would produce a higher yield. A yield curve inversion and the bond rates that come along with it can upend the bond market and may portend worse economic conditions to come.

- A flat yield curve falls between a normal and an inverted yield curve. When market conditions cause yield curves to change from normal to inverted, or vice versa, they pass through a transitional period where nearly all the bond terms produce roughly the same yield. If the economy is transitioning from growth to contraction, the long-term yields will fall and the short-term yields will rise, creating this flattening effect en route to an eventual yield curve inversion. But eventually, the economy will return to growth and bond yields will return to normal conditions, passing through another flat yield curve along the way.

How to Interpret the Yield Curve

When the treasury yield curve is normal, it indicates investor confidence in future economic growth. However, this does not mean that savvy investors rush off to park their money in the longest-term bonds, even though they offer the highest interest rates.

- In a normal yield curve, there often isn’t a massive difference in the long-term yields offered by a 30-year bond versus the yields offered by a 5-year bond. Therefore, many investors will opt for the shorter-term 5-year bond, reclaim their money at the end of those five years, and look for something new to invest in, such as stocks or real estate or new treasury notes. Yet some people stay out of the bond market entirely during a normal yield curve, because while bonds pay decently in a growing economy, stocks tend to pay even more.

- When the yield curve inverts, it means that investors and economists are pessimistic about long-term economic growth. The advantage to bond investing, however, is that you get locked into an interest rate when you purchase debt security—which is a good thing if the economy is trending downward. Therefore, in the early days of a yield curve inversion, many investors will try to buy up long term bonds before they decrease further in value. While they aren’t acquiring those bonds at their peak rate, they are nonetheless guaranteed some degree of economic certainty since the long-term bonds will pay their promised interest rates, even if overall economic activity declines further.

How Can Term Structure and the Yield Curve Be Used to Judge the Health of the Credit Market?

The term structure of interest rates, which tracks the interest rates of savings bonds, is often used to predict economic expansion and economic recession. That said, bond investing is only one component of a nation’s overall economic activity. The stock market is another important component. Perhaps most important is the job market, since most people—from the U.S. to Europe to China—derive most of their income from wages, not investments.

- Nonetheless, the yield curve is considered an incredibly important economic indicator. Financial journalism pays special deference to the yield curve as a symbolic representation of the economy at large. In fact, the yield curve is used as a benchmark for other debt in the market. This includes mortgage rates and bank lending rates, even those are also steered by the monetary policy of a central bank, such as the United States Federal Reserve.

- On Wall Street, the yield curve is used to predict changes in economic output and growth. The bond yields of both short-term and long-term debt securities tend to reveal a lot about the overall state of the U.S. economy, and the economy of any nation where government-issued debt is considered reliable investment security.

One thing that the yield curve teaches us about the credit market is that investors have a liquidity preference—this is to say they like the freedom to easily move their money around. Such a concept is outlined in the liquidity premium theory, which states that investors are willing to pay a premium in the form of lower interest returns in exchange for the privilege of not having their money trapped in long term bonds. This means that short term bonds can get away with paying less interest than long term bonds; consumers accept the lower rates in exchange for the ability to cash out more rapidly.

The inverse is also true: bond managers often have to promise higher interest rates in order to entice people to invest in longer-term securities. If the rate of interest isn’t high enough to entice them, investors will instead park their money in shorter-term assets, so that they have the option of easily moving it to another investment after a short amount of time has passed.

Learn more about economics and society in Paul Krugman’s MasterClass.

What Is the Term Structure of Interest Rates?

The term structure of interest rates is a comparison tool that plots the term length of investment securities against the amount of interest they pay. In economic circles, the term structure of interest rates is frequently referred to as a yield curve.