Learn About Recessions: Causes, Effects, and How America Overcame the Great Recession of 2008

Written by MasterClass

Last updated: Oct 12, 2022 • 10 min read

The Great Recession of 2008 had a lot of people questioning what a recession was—and why it happened in the first place. History provides invaluable lessons to economists who study economic downturns and upturns, but it is also important for the average citizen to understand how consumer behavior may impact markets, especially those that end up in a significant decline.

Learn From the Best

What Is a Recession?

A recession is a slowdown or contraction of the economy over a business cycle. The period of time and what exactly indicates an economic recession are not tightly defined. Some countries and economists define a recession as a contraction over two consecutive quarters, some define it as six months, and some do not define the time period at all, taking a more complete and nuanced view of different data points to indicate a recession.

What Is the Difference Between a Recession and a Depression?

The difference between a recession and a depression largely comes down to severity. While there’s no set definition, a depression can be thought of as an extended recession that lasts for an extraordinarily long time—years, rather than months or quarters. The Great Depression, for instance, ran from 1929 until the beginning of World War II. By comparison, the so-called “Great Recession” of 2007-2009 lasted 18 months.

What Causes a Recession?

Some recessions can be traced to a clearly-defined cause. For instance, the recession of 1973-1975 began as a result of the 1973 oil crisis. However, most recessions are caused by a complex combination of factors, including high interest rates, low consumer confidence, and stagnant wages or reduced real income in the labor market. Other examples of recession causes include bank runs and asset bubbles (see below for an explanation of these terms).

What Are the Indicators of a Recession?

Economists determine whether an economy is in recession by looking at a variety of statistics and trends. Factors that indicate a recession include:

- Rising in unemployment

- Rises in bankruptcies, defaults, or foreclosures

- Falling interest rates

- Lower consumer spending and consumer confidence

- Falling asset prices, including the cost of homes and dips in the stock market

All of these factors can lead to an overall reduction in the Gross Domestic Product (GDP). The European Union and the United Kingdom define a recession as two or more consecutive quarters of negative real GDP growth.

In the United States, the National Bureau of Economic Research (NBER) tracks multiple economic indicators, including those listed above, to determine whether the US economy is in recession. For example, the NBER declared a recession in the early 1990s, even though the GDP contracted inconsistently over three non-consecutive quarters.

Paul Krugman uses babysitting as an example to illustrate what happens to the economy during a recession.

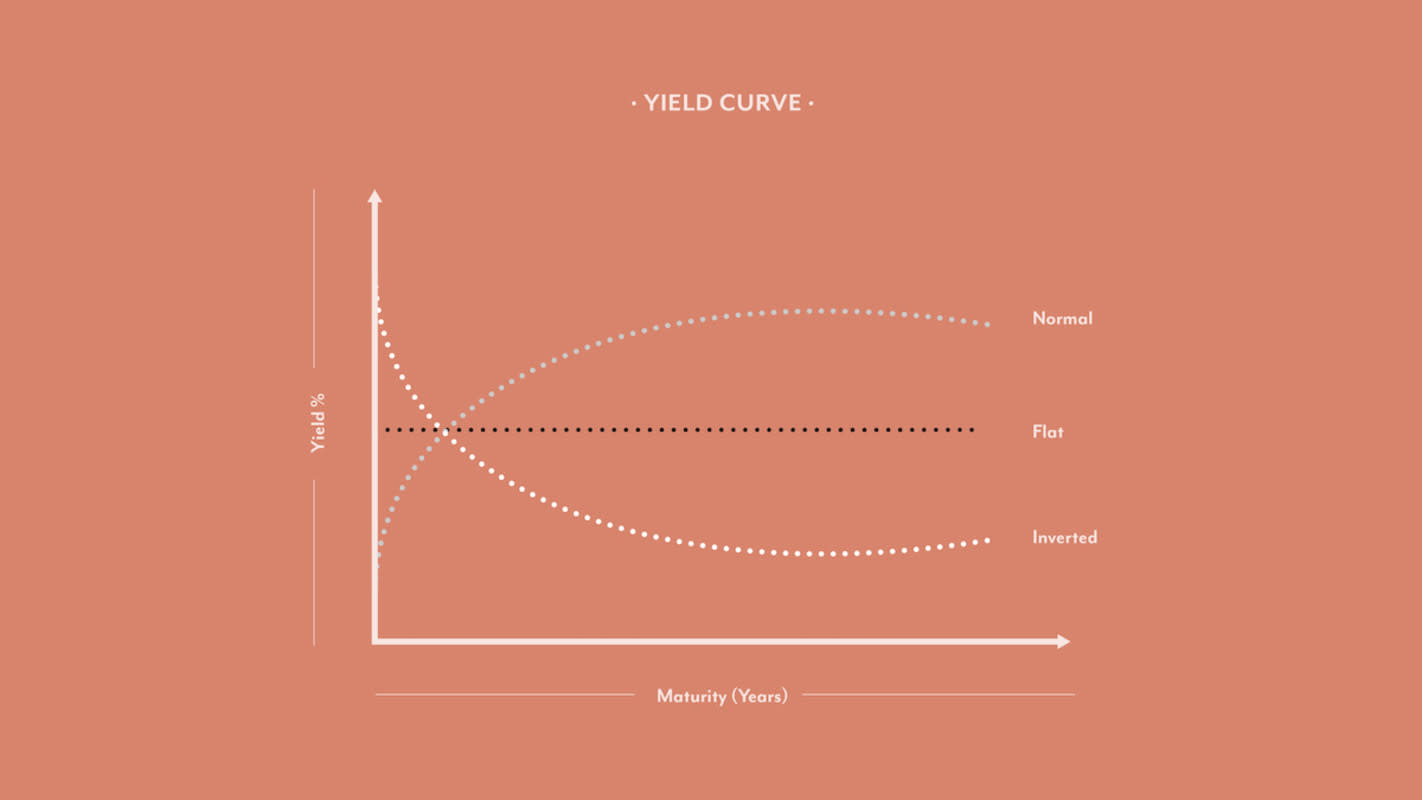

The Yield Curve as an Indicator of Recession

The yield curve is another indicator of recessions, and one the NBER uses to predict or declare a recession.

A yield curve is a line on a graph that tracks the interest rates of bonds that are equal in credit, but have different times at which they mature. A common yield curve looks at US Treasury Debt at three month, two year, five year, ten year, and 30 year maturity benchmarks.

There are three different types, or shapes, of a yield curve that indicate different stages of economic expansion and contraction:

- 1. Normal. A normal yield curve means that longer term bonds have a higher yield than short term bonds. This is expected behavior, and generally indicates a healthy economy and a positive economic growth rate.

- 2. Flat. A flat yield curve means that longer term bonds are beginning to have yields that are about the same as those for short term yields. This means that the economy is in transition, or approaching a recession, as investors are locking in longer term bond rates before they decline further.

- 3. Inverted. An inverted yield curve is one where longer term bonds have a lower yield than short term bonds. This is an indicator of a recession, as it suggests that interest rates are falling or will continue to drop.

How Do Banks Contribute to Recession?

Consumer confidence is key to keeping banks, and their processes, in equilibrium. After the Wall Street stock market crashed in 1929, panic spread, and consumers began pulling money out of banks, further worsening the situation (which we now know resulted in the Great Depression).

How Do Banks Work?

Banks take in deposits from their customers and lend those deposits out to borrowers. The banks promise depositors that they can get their money back whenever they want, and at the same time, promise borrowers that they only have to repay their loan slowly on a fixed schedule. This system gives both depositors and borrowers the sense of certainty they need to plan their lives. But to accomplish this the bank, must absorb and then manage a very specific type of risk: the risk of a run.

What Is a Bank Run?

If all of a bank’s depositors decided to withdraw their money on the same day, the bank would not be able to honor all or even most of the requests. Normally, of course, this would be extremely unlikely. However, it can as a result of a self-fulfilling prophecy known as a “bank run.”

Suppose that, rightly or wrongly, depositors become afraid that the bank has made bad loans and will soon not have enough money to honor its deposits. The depositors rush to take their savings out before the bank runs out of money. Other depositors see this happening, and rush to join first wave of depositors. Soon, every depositor is asking for their money back, and the bank is unable to honor all of the withdrawals. If a bank run happens at one bank, it can frighten customers at another bank, causing a bank run there as well. This can soon lead to a cascade of bank failures.

Waves of bank failures occurred during the Great Depression. After the Depression, the government founded the FDIC to insure deposits, and required banks to follow strict safety guidelines. Slowly, however, new financial institutions appeared that weren’t officially banks, but nonetheless made their money by taking bank-like risks. These institutions created a shadow banking system, and by 2008 they handled almost ten times more money than the regular banking system.

What Are Asset Bubbles?

Bank runs are often associated with asset bubbles.

The fundamental value of an asset is the return (or profit) an investor believes he or she would receive if he or she bought an asset, then sold it at a later date. For real estate, the fundamental value is based on rent the property will earn over its lifetime. For stocks, the fundamental value is based on profits the company will earn. Asset bubbles occur when investors are willing to pay far more than a reasonable estimate of fundamental value, in the hopes that they will be able to sell the asset later to other investors for even more money.

After a while, the flow of new investors in these assets slows. As finding new investors becomes more difficult, old investors panic and sell their assets all at once. This is sometimes called a Wile E. Coyote moment, after the famous cartoon character who would run off a cliff but only begin to fall when he noticed the ground was no longer beneath him. In the same way, the price of an asset in a bubble continues to rise above its fundamental value until investors notice that they are running out of new investors to whom they can sell.

How Do You Fix a Recession?

In most cases, governments can mitigate and reverse downturns by printing more money, then effectively loaning it out at low interest rates. These lower interest rates make it easier for households and businesses to borrow money from banks. In turn, the additional loans banks are able to inject more money into the economy, thereby allowing it to recover from the recession.

What Is the Zero Lower Bound?

The recession-fighting strategies above face an important limitation: the zero lower bound.

- When interest rates approach zero, increases in the supply of currency has no effect. Households and businesses no longer have an increased incentive to take out loans, which means the extra money that was printed sits in banks without being spent.

- If the economy reaches the zero lower bound during a recession, it is said to be in a “liquidity trap.”

- The Federal Reserve (the central bank of the United States) would like to increase economic activity to bring the economy out of recession, but is unable to do so because its primary tool, liquidity (i.e., printing more money), is no longer effective.

Read more about inflation and the IS-LM model, which outlines when a liquidity trap occurs.

The Economic Downturn and the Great Recession of 2008

In 2008, the United States entered the worst recession in 75 years, and the rest of the world soon followed. Many other economists had become complacent about the possibility of not just garden-variety recessions, but the type of major recessions caused by banking crises.

How Did the Great Recession of 2008 Start?

The subprime financial crisis in 2008 combined elements of an asset bubble with a bank run. The shadow banking system took loans from subprime borrowers, then combined thousands of those loans into a single pool. As long as all borrowers didn’t default at once, the pool would collect a predictable number of payments each month. When the housing bubble burst, however, many of the subprime borrowers defaulted all at once, and payments into the pools stopped. Without that income, shadow banks such as Accredited Home Loans or Freedom Mortgage Company could not honor their obligations.

Shadow banks were providing a lot of the economy’s credit. When they went down, that credit was cut off. This caused spending in the economy to fall, which led to a drop in prices of not only the housing market, but commercial property, automobiles, and other assets. These drops in prices made it even more difficult for borrowers to get or repay loans, which led to further declines in spending and prices.

Economists refer to this type of crisis as “debt deflation,” and it is too large even for the Fed to stop. As a result of this snowball effect, unemployment soared from 4.5% to around 10%. An unemployment rate of 10% meant that roughly 15 million Americans who wanted to find a job could not. Now referred to as the Great Recession, this was the worst economic crisis since the Great Depression. Retail sales and industrial production slowed, and millions of manufacturing workers lost their jobs, though not as a result of anything that the workers or their employers did.

The crisis of 2008 negatively impacted millions of people. The massive job loss and potential scarring of entire career paths means that a recession is more than just an abstract economic concept. Recessions take an enormous toll on those who live through them.

How Was the Great Recession of 2008 Fixed?

When the Great Recession began in the United States, Ben Bernanke, the Chairman of the Federal Reserve, was aware that there was only a very small chance that he would be able to turn around the United States economy before it hit the liquidity trap. Bernanke responded by printing money aggressively. Economists and other commentators who were not familiar with Japan’s experience became frightened that he would cause extreme inflation. However, most of the money sat in banks and did not circulate in the wider economy.

- Despite the huge increase in the money supply, prices increased only slightly. Bernanke’s efforts had helped slow the economic collapse, but the shock the financial system experienced was too great to be overcome entirely. The United States found itself in a liquidity trap, which meant the Fed’s monetary policy tools were useless.

- To address this problem, President Obama enacted a fiscal policy in 2009 known as the American Recovery and Reinvestment Act. This stimulus plan contained approximately $288 billion in tax cuts and $499 billion in spending. That plan, combined with Bernanke’s efforts, prevented the United States from repeating the Great Depression. Though it wasn’t strong enough to avoid the liquidity trap completely, it was able to alter the economy’s trajectory.

- When the Great Recession first began in 2007, it was following nearly exactly the same track as the Great Depression. Yet, by early 2010, the descent leveled off. The unemployment rate peaked at 10 percent in October of 2009 and hovered around 9.9 percent until April of 2010, when it dropped to 9.6%. From there it began a downward trend that so far has lasted through the summer of 2018.

- The downturn was difficult, but for the United States, it didn’t approach the depths that occurred during the Great Depression.

Want to Learn More About Economics?

Learning to think like an economist takes time and practice. For Nobel Prize-winner Paul Krugman, economics is not a set of answers—it’s a way of understanding the world. In Paul Krugman’s MasterClass on economics and society, he talks about the principles that shape political and social issues, including access to health care, the tax debate, globalization, and political polarization.

Want to learn more about economics? The MasterClass Annual Membership provides exclusive video lessons from master economists and strategists, like Paul Krugman.